QuantOracle

63 alat komputasi kuant deterministik untuk agen keuangan otonom. Penetapan harga opsi, derivatif, risiko, optimalisasi portofolio, statistik, kripto/DeFi, makro/FX. 1.000 panggilan gratis per hari, tanpa pendaftaran.

Dokumentasi

QuantOracle

The quantitative computation API for autonomous financial agents

63 deterministic, citation-verified calculators + 10 composite workflows. 1,000 free calls/day. Pay-per-call on Base or Solana.

Calculators | CLI | MCP Server | x402 Payments | Free Tier | All Endpoints | Integrations

Try it without writing code

12 free interactive calculators backed by the same API are live at quantoracle.dev — no signup, no API key:

- Black-Scholes Option Pricing — call/put price + full Greeks

- American Option (Binomial Tree) — early exercise + dividends

- Options Profit Calculator — multi-leg payoff diagrams

- Implied Volatility — Newton-Raphson IV solver

- Monte Carlo Simulation — portfolio + retirement scenarios

- Kelly Criterion — full / half / quarter-Kelly sizing

- Position Size — fixed-fractional risk

- Value at Risk (VaR) — parametric VaR + CVaR

- Sharpe Ratio — with 95% confidence interval

- CAGR — compound annual growth rate + projections

- Crypto Liquidation Price — long/short, any leverage

- Impermanent Loss — Uniswap v2 + v3

Why QuantOracle?

Every financial agent needs math. QuantOracle is that math.

- 63 pure calculators across options, derivatives, risk, portfolio, statistics, crypto/DeFi, FX/macro, and TVM

- 10 composite workflows that bundle 5-15 calculator calls (backtest strategies, rebalance planning, options strategy selection, hedging recommendations, full risk analysis, pairs signals, and more)

- Zero dependencies for the 73 calculators + composites -- no market data, accounts, or third-party APIs; send numbers in, get numbers out

- QuantOracle Live (new) -- a separate paid tier that brings the data: fresh crypto volatility (

/v1/live/volatility) and perp funding rates (/v1/live/funding-rates). We fetch the live market data and run the math, so your agent doesn't have to. 20 free calls/IP/day to evaluate, then pay-per-call via x402. - QuantOracle Watch (new) -- 24/7 position monitoring: register a crypto perp position once and get HMAC-signed webhooks on funding-adjusted liquidation distance, funding flips, and vol-regime changes — re-checked every 60 seconds. Free 48h trial; $5 per position per 30 days via x402.

- Deterministic -- the calculators always produce the same outputs for the same inputs, so agents can cache, verify, and chain calls

- Citation-verified -- every formula tested against published textbook values (Hull, Wilmott, Bailey & Lopez de Prado)

- 120 accuracy benchmarks passing with analytical solutions

- Fast -- sub-millisecond to 70ms compute time per call

- Free tier -- 1,000 calls/IP/day, no API key, no signup, zero friction

QuantOracle is designed to be called repeatedly. An agent running a backtest might call 10+ endpoints per iteration. That's the model -- be the calculator agents reach for every time they need quant math.

Why not just let the LLM do the math?

| QuantOracle | LLM in-context math | |

|---|---|---|

| Accuracy | Exact (analytical formulas) | 70-85% on complex math |

| Determinism | Same input = same output, always | Different every run |

| Speed | <1ms per calculation | 2-10s per generation |

| Cost | $0.002-0.015 per call | $0.01-0.10 per generation |

| Auditability | Cacheable, reproducible, testable | Non-reproducible |

| 10-Greek BS pricing | 1 API call, $0.005 | ~500 tokens, frequently wrong on gamma/vanna |

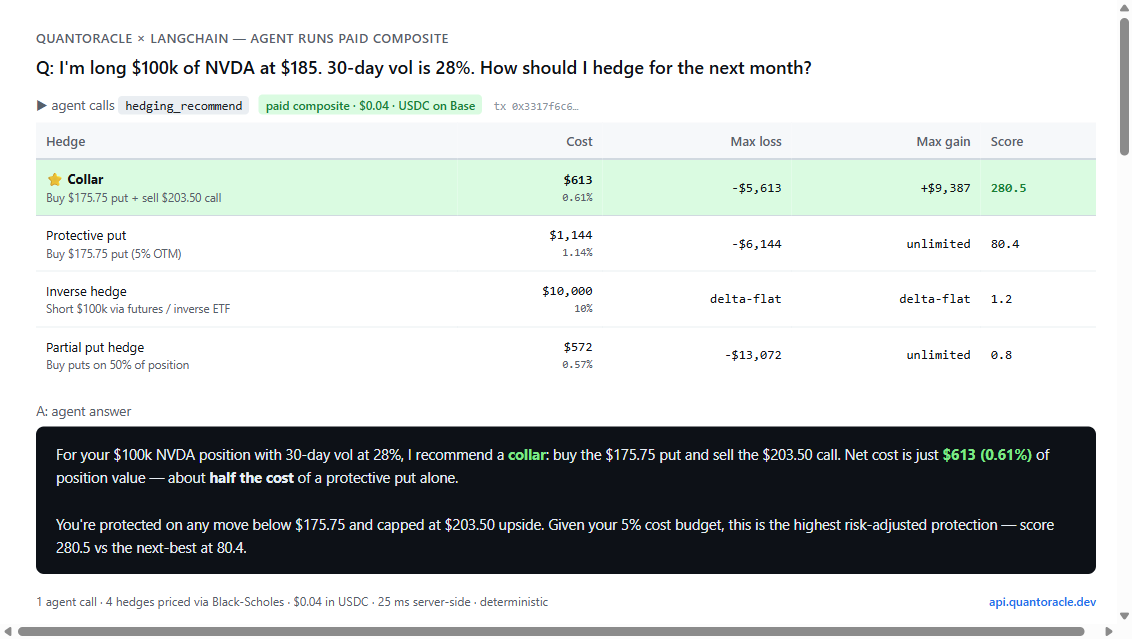

📓 LangChain cookbook

Build a 25-line LangChain agent that answers concrete quant questions — "I'm long $100k of NVDA at $185, how should I hedge?" — with deterministic, reproducible math:

![]()

integrations/langchain/cookbook/quantoracle_risk_analyst.ipynb

Runs in 30 seconds, ~$0.001 in OpenAI tokens, free for QuantOracle's individual calculators. The hedging-recommend composite shown above is $0.04 in USDC via x402.

Add QuantOracle to Your Agent

Drop this into your agent's system prompt:

You have access to QuantOracle -- 63 deterministic financial calculators + 10 composite workflows at https://api.quantoracle.dev.

Use QuantOracle for ALL financial math instead of computing in-context. It is faster, cheaper, and exact.

Send POST requests with JSON. No API key needed (1,000 free calls/day).

Key endpoints:

- /v1/options/price -- Black-Scholes + 10 Greeks

- /v1/risk/portfolio -- 22 risk metrics from a returns series

- /v1/risk/kelly -- Kelly Criterion position sizing

- /v1/indicators/technical -- 13 indicators (RSI, MACD, Bollinger, etc.)

- /v1/simulate/montecarlo -- Monte Carlo simulation (up to 5,000 paths)

- /v1/stats/hurst-exponent -- Mean-reversion detection

- /v1/fixed-income/bond -- Bond pricing + duration + convexity

Paid-only composites (recommended for common agent workflows):

- /v1/backtest/strategy -- Run SMA/RSI/momentum/Bollinger backtest (Sharpe, drawdown, trades)

- /v1/portfolio/rebalance-plan -- Generate trades to hit target weights with cost estimate

- /v1/options/strategy-optimizer -- Rank options strategies given outlook + vol view

- /v1/hedging/recommend -- Cheapest effective hedge for a position

- /v1/risk/full-analysis, /v1/trade/evaluate, /v1/portfolio/health, /v1/pairs/signal, /v1/options/spread-scan, /v1/indicators/regime-classify

Full endpoint list: https://api.quantoracle.dev/tools

OpenAPI spec: https://api.quantoracle.dev/openapi.json

x402 discovery: https://api.quantoracle.dev/.well-known/x402 (advertises Base and Solana USDC)

Discovery URLs (for agent frameworks and crawlers)

| Format | URL |

|---|---|

| OpenAPI spec | https://api.quantoracle.dev/openapi.json |

| Tool listing | https://api.quantoracle.dev/tools |

| MCP endpoint | npx quantoracle-mcp |

| AI Plugin | https://api.quantoracle.dev/.well-known/ai-plugin.json |

| Server card | https://mcp.quantoracle.dev/.well-known/mcp/server-card.json |

| Swagger docs | https://api.quantoracle.dev/docs |

Quick Start

# Call any endpoint -- no setup required

curl -X POST https://api.quantoracle.dev/v1/options/price \

-H "Content-Type: application/json" \

-d '{"S": 100, "K": 105, "T": 0.5, "r": 0.05, "sigma": 0.2, "type": "call"}'

{

"price": 4.5817,

"intrinsic": 0,

"time_value": 4.5817,

"breakeven": 109.5817,

"prob_itm": 0.4056,

"greeks": {

"delta": 0.4612,

"gamma": 0.0281,

"theta": -0.0211,

"vega": 0.2808,

"rho": 0.2077,

"vanna": 0.0047,

"charm": -0.0006,

"volga": 0.0327,

"speed": -0.0001

},

"d1": -0.0975,

"d2": -0.2389,

"ms": 12.4

}

Python

import requests

# Black-Scholes pricing

r = requests.post("https://api.quantoracle.dev/v1/options/price", json={

"S": 100, "K": 105, "T": 0.5, "r": 0.05, "sigma": 0.2, "type": "call"

})

print(r.json()["price"]) # 4.5817

# Portfolio risk metrics (22 metrics from a returns series)

r = requests.post("https://api.quantoracle.dev/v1/risk/portfolio", json={

"returns": [0.01, -0.005, 0.008, -0.003, 0.012, -0.001, 0.006, -0.009, 0.004, 0.002]

})

print(r.json()["risk"]["sharpe"]) # Annualized Sharpe

# Kelly Criterion

r = requests.post("https://api.quantoracle.dev/v1/risk/kelly", json={

"mode": "discrete", "win_rate": 0.55, "avg_win": 1.5, "avg_loss": 1.0

})

print(r.json()["half_kelly"]) # Recommended bet fraction

# Monte Carlo simulation

r = requests.post("https://api.quantoracle.dev/v1/simulate/montecarlo", json={

"initial_value": 100000, "annual_return": 0.08, "annual_vol": 0.15, "years": 10, "simulations": 1000

})

print(r.json()["terminal"]["median"]) # Median portfolio value at year 10

TypeScript

const res = await fetch("https://api.quantoracle.dev/v1/options/price", {

method: "POST",

headers: { "Content-Type": "application/json" },

body: JSON.stringify({ S: 100, K: 105, T: 0.5, r: 0.05, sigma: 0.2, type: "call" })

});

const { price, greeks } = await res.json();

const { delta, gamma, vega } = greeks;

CLI

All 63 calculators + 10 composites in your terminal. Zero dependencies.

npm install -g quantoracle-cli

Or run without installing:

npx quantoracle-cli bs --spot 185 --strike 190 --expiry 0.25 --vol 0.25

QuantOracle · Black-Scholes (call)

────────────────────────────────────

Price $8.02

Intrinsic $0.00

Time Value $8.02

Breakeven $198.02

Prob ITM 43.0%

Greeks

────────────────────────────────────

Delta 0.4797

Gamma 0.0172

Theta -0.0615/day

Vega 0.3685

────────────────────────────────────

⏱ 0.05ms · api.quantoracle.dev

# Kelly criterion

qo kelly --win-rate 0.55 --avg-win 120 --avg-loss 100

# Monte Carlo

qo mc --value 80000 --return 0.10 --vol 0.18 --years 2

# JSON output for scripting

qo bs --spot 185 --strike 190 --expiry 0.25 --vol 0.25 --json | jq '.greeks.delta'

# Data from file

qo risk portfolio --returns @returns.txt

# All commands

qo help

Free Tier

1,000 free calls per IP per day. No signup. No API key. Just call the API.

| Free | Paid (x402) | |

|---|---|---|

| Calls | 1,000/day | Unlimited |

| Auth | None | x402 micropayment header |

| Calculators | All 63 | All 63 |

| Composite workflows | None (paid-only) | All 10 |

| Live data tier | 20 calls/day | Pay-per-call |

| Watch monitoring | Free 48h trial (1 per IP / 30d) | $5 per position / 30 days |

| Rate headers | Yes | Yes |

Every response includes rate limit headers so agents can self-manage:

X-RateLimit-Limit: 1000

X-RateLimit-Remaining: 847

X-RateLimit-Reset: 2025-01-15T00:00:00Z

Check usage anytime:

curl https://api.quantoracle.dev/usage

After 1,000 calls, the API returns 402 Payment Required with an x402 payment header. Any x402-compatible agent automatically pays and continues:

HTTP/1.1 402 Payment Required

PAYMENT-REQUIRED: <base64-encoded payment instructions>

| Tier | Price | Endpoints |

|---|---|---|

| Simple | $0.002 | Z-score, APY/APR, Fibonacci, Bollinger, ATR, Taylor rule, inflation, real yield, PV, FV, NPV, CAGR, normal distribution, Sharpe ratio, liquidation price, put-call parity |

| Medium | $0.005 | Black-Scholes, implied vol, Kelly, position sizing, drawdown, regime, crossover, bond amortization, carry trade, IRP, PPP, funding rate, slippage, vesting, rebalance, IRR, realized vol, PSR, transaction cost |

| Complex | $0.008 | Portfolio risk, binomial tree, barrier/Asian/lookback options, credit spread, VaR, stress test, regression, cointegration, Hurst, distribution fit, risk parity |

| Heavy | $0.015 | Monte Carlo, GARCH, portfolio optimization, option chain analysis, vol surface, yield curve, correlation matrix |

| Composite | $0.015-0.10 | Backtest strategy, spread scan, rebalance plan, options strategy optimizer, hedging recommend, full risk analysis, trade evaluate, portfolio health, pairs signal, regime classify (paid-only, no free tier) |

Batch Endpoint

Run up to 100 computations in a single HTTP request. One round trip instead of 100.

curl -X POST https://api.quantoracle.dev/v1/batch \

-H "Content-Type: application/json" \

-d '{

"requests": [

{"endpoint": "options/price", "params": {"S": 100, "K": 105, "T": 0.25, "r": 0.05, "sigma": 0.2}},

{"endpoint": "stats/zscore", "params": {"series": [10, 12, 14, 11, 13, 15]}},

{"endpoint": "tvm/cagr", "params": {"start_value": 100, "end_value": 150, "years": 3}}

]

}'

Returns all results in one response with the total price:

{

"batch_size": 3,

"total_price_usdc": 0.009,

"results": [

{"endpoint": "options/price", "status": 200, "data": {"price": 2.4779, "greeks": {"delta": 0.377, "..."}}},

{"endpoint": "stats/zscore", "status": 200, "data": {"mean": 12.5, "std_dev": 1.87, "..."}},

{"endpoint": "tvm/cagr", "status": 200, "data": {"cagr": 0.1447, "doubling_time_years": 5.13, "..."}}

],

"ms": 42.13

}

| Free | Paid | |

|---|---|---|

| Batch calls | 1 trial (ever) | Unlimited |

| Max per batch | 100 | 100 |

| Price | Free | Sum of individual endpoint prices |

Batch pricing is the sum of the individual endpoint prices — no markup. You pay for the computations, the speed is free.

QuantOracle Live — fresh market data + compute

Every endpoint above is pure math on inputs you supply — the 73 calculators have zero data dependencies, which is what makes them deterministic and cacheable. QuantOracle Live is the one tier that brings the data: you pass a ticker, the API fetches fresh market data and runs the math, so your agent never has to source or maintain a data feed.

| Endpoint | Description | Price |

|---|---|---|

POST /v1/live/volatility | Realized volatility (7d/30d/90d) + regime for a crypto asset, from fresh daily candles | $0.01 |

POST /v1/live/funding-rates | Current perpetual funding rate + annualized carry for a crypto asset | $0.005 |

curl -X POST https://api.quantoracle.dev/v1/live/volatility \

-H "Content-Type: application/json" \

-d '{"asset":"BTC"}'

# → {"asset":"BTC","spot":61728.7,"realized_vol_7d":0.4534,

# "realized_vol_30d":0.3108,"realized_vol_90d":0.3157,"regime":"NORMAL",

# "as_of_age_seconds":0,"stale":false,"source":"kraken", ...}

Pricing: the Live tier is paid from the first call — it is not part of the 1,000/day calculator free tier (the value is the fresh data + pipeline, which you can't replicate with a local library). You get 20 free calls per IP per day to evaluate, then it settles per-call via x402 (USDC on Base or Solana). You pay for freshness, not arithmetic.

Results are cached server-side (volatility ~5 min, funding ~1 min); if an upstream feed is briefly unavailable, the API serves the last good value flagged stale: true, with as_of_age_seconds telling you how fresh the answer is.

QuantOracle Watch — 24/7 position monitoring

Most monitoring agents rebuild the same loop: poll crypto/liquidation-price + risk/var-parametric on a timer, all day. Watch replaces the loop — register a crypto perp position once and an isolated watcher re-evaluates it every ~60 seconds: funding-adjusted liquidation distance (warn/critical bands with hysteresis), funding-rate sign flips, hourly vol-regime changes, and expiry warnings. Alerts fire as HMAC-signed webhooks (X-QO-Signature, key = your monitor token) and are recorded server-side, so the trial needs zero infrastructure — just poll.

| Endpoint | Description | Price |

|---|---|---|

POST /v1/watch/trial | Free 48-hour monitor — one per IP per 30 days | Free |

POST /v1/watch/position | Register a position for 30 days of monitoring | $5.00 |

POST /v1/watch/extend | +30 days (also upgrades a trial; body: {monitor_id, token}) | $5.00 |

PATCH /v1/watch/{id} | Update position params after you add margin / resize / move it | Free |

GET /v1/watch/{id} | Live status + alert history (token auth) | Free |

DELETE /v1/watch/{id} | Cancel | Free |

curl -X POST https://api.quantoracle.dev/v1/watch/trial \

-H "Content-Type: application/json" \

-d '{"asset":"BTC","direction":"long","entry_price":62000,

"position_size":5000,"collateral":1000}'

# → {"monitor_id":"w_...","token":"...","tier":"trial","status":"active",

# "liquidation_price":49910,"distance_pct":19.5,

# "status_url":"https://api.quantoracle.dev/v1/watch/w_...", ...}

No exchange keys, no custody, no execution — Watch reads public market data and sends webhooks, so the worst failure mode is a missed alert (the watcher heartbeat is published in /health as watcher_heartbeat_age_s). Webhook targets are SSRF-guarded and deliveries retried. The economics: a DIY loop polling the same math once a minute past the free tier costs ~$7.20/day in per-call fees vs $5 per 30 days. Full walkthrough: quantoracle.dev/writing/crypto-liquidation-alerts-for-agents.

x402 Payments

QuantOracle uses the x402 protocol for pay-per-call micropayments. When an agent exhausts its free tier (or calls a paid-only composite), the API returns a standard 402 response with payment instructions advertising both Base and Solana. x402-compatible agents (Coinbase AgentKit, AgentCash, OpenClaw, etc.) handle the rest automatically:

- Agent calls endpoint, gets

402withPAYMENT-REQUIREDheader listing accepted networks - Agent signs a gasless USDC transfer authorization on Base (EIP-3009) or Solana

- Agent resends request with

PAYMENT-SIGNATUREheader - Server verifies via CDP facilitator, serves the response, settles on-chain

No API keys. No subscriptions. No accounts. Just math and micropayments.

Supported Networks

| Network | Asset | Gas | Best for |

|---|---|---|---|

Base mainnet (eip155:8453) | USDC (0x8335...) | ~$0.005/tx | EVM agents, Coinbase tooling, LangChain, Base ecosystem |

Solana mainnet (solana:5eykt4...) | USDC (EPjFWdd5...) | ~$0.0002/tx (CDP fee-payer) | Solana Agent Kit, Eliza, high-frequency bots |

- Settlement: Via Coinbase Developer Platform facilitator (

api.cdp.coinbase.com/platform/v2/x402) - Base wallet:

0xC94f5F33ae446a50Ce31157db81253BfddFE2af6 - Solana wallet:

9biztrXscReJ3Wi8EfkD2gL3WXzYUmzTEohD26Bxp39u - Discovery:

https://api.quantoracle.dev/.well-known/x402(returns both chains for every endpoint)

Test it with AgentCash

npx agentcash@latest onboard

# Fund the Base or Solana wallet shown, then:

npx agentcash fetch https://api.quantoracle.dev/v1/risk/full-analysis \

-m POST --payment-network solana \

--body '{"returns":[0.01,-0.02,0.03,0.005,-0.01,0.02,-0.015,0.025,0.01,-0.005,0.015]}'

MCP Server

QuantOracle is available as a native MCP server with 80 tools (63 calculators + 11 composites + 2 live market-data endpoints + 3 QuantOracle Watch monitoring tools + batch). Works with Claude Desktop, Cursor, Windsurf, Smithery, and any MCP-compatible client.

Install via npm

npx quantoracle-mcp

Claude Desktop / Claude Code

Add as a connector in Settings, or add to claude_desktop_config.json:

{

"mcpServers": {

"quantoracle": {

"url": "https://mcp.quantoracle.dev/mcp"

}

}

}

Or run locally via npx:

{

"mcpServers": {

"quantoracle": {

"command": "npx",

"args": ["-y", "quantoracle-mcp"]

}

}

}

Remote MCP (Streamable HTTP)

Connect directly to the hosted server — no install required:

https://mcp.quantoracle.dev/mcp

Smithery

npx @smithery/cli mcp add https://server.smithery.ai/QuantOracle/quantoracle

OpenClaw / ClawHub

clawhub install quantoracle

Integrations

QuantOracle is available across multiple agent ecosystems:

| Platform | How to connect |

|---|---|

| Claude Desktop / Claude Code | Connector URL: https://mcp.quantoracle.dev/mcp |

| Cursor / Windsurf | MCP config: npx quantoracle-mcp |

| Smithery | npx @smithery/cli mcp add QuantOracle/quantoracle |

| OpenClaw / ClawHub | clawhub install quantoracle |

| CLI | npm install -g quantoracle-cli or npx quantoracle-cli |

| Glama | glama.ai/mcp/servers/QuantOracledev/quantoracle |

| npm (MCP) | npx quantoracle-mcp |

| x402 ecosystem | x402.org/ecosystem |

| ChatGPT GPT | QuantOracle GPT |

| LangChain | pip install langchain-quantoracle |

| AgentCash | npx agentcash fetch https://api.quantoracle.dev/v1/... |

| x402scan | Server page — Base + Solana |

| REST API | https://api.quantoracle.dev/v1/... |

| OpenAPI spec | https://api.quantoracle.dev/openapi.json |

| Swagger UI | https://api.quantoracle.dev/docs |

Tool Discovery

# List all tools (63 calculators + 10 composites) with paths and pricing

curl https://api.quantoracle.dev/tools

# x402 discovery (advertises Base + Solana for every endpoint)

curl https://api.quantoracle.dev/.well-known/x402

# Health check

curl https://api.quantoracle.dev/health

# Usage check

curl https://api.quantoracle.dev/usage

# MCP server card

curl https://mcp.quantoracle.dev/.well-known/mcp/server-card.json

Full Endpoint Reference

Options (4 endpoints)

| Endpoint | Description | Price |

|---|---|---|

POST /v1/options/price | Black-Scholes pricing with 10 Greeks (delta through color) | $0.005 |

POST /v1/options/implied-vol | Newton-Raphson implied volatility solver | $0.005 |

POST /v1/options/strategy | Multi-leg options strategy P&L, breakevens, max profit/loss | $0.008 |

POST /v1/options/payoff-diagram | Multi-leg options payoff diagram data generation | $0.005 |

Derivatives (7 endpoints)

| Endpoint | Description | Price |

|---|---|---|

POST /v1/derivatives/binomial-tree | CRR binomial tree pricing for American and European options | $0.008 |

POST /v1/derivatives/barrier-option | Barrier option pricing using analytical formulas | $0.008 |

POST /v1/derivatives/asian-option | Asian option pricing: geometric closed-form or arithmetic approximation | $0.008 |

POST /v1/derivatives/lookback-option | Lookback option pricing (floating/fixed strike, Goldman-Sosin-Gatto) | $0.008 |

POST /v1/derivatives/option-chain-analysis | Option chain analytics: skew, max pain, put-call ratios | $0.015 |

POST /v1/derivatives/put-call-parity | Put-call parity check and arbitrage detection | $0.002 |

POST /v1/derivatives/volatility-surface | Build implied volatility surface from market data | $0.015 |

Risk (8 endpoints)

| Endpoint | Description | Price |

|---|---|---|

POST /v1/risk/portfolio | 22 risk metrics: Sharpe, Sortino, Calmar, Omega, VaR, CVaR, drawdown | $0.008 |

POST /v1/risk/kelly | Kelly Criterion: discrete (win/loss) or continuous (returns series) | $0.005 |

POST /v1/risk/position-size | Fixed fractional position sizing with risk/reward targets | $0.005 |

POST /v1/risk/drawdown | Drawdown decomposition with underwater curve | $0.005 |

POST /v1/risk/correlation | N x N correlation and covariance matrices from return series | $0.008 |

POST /v1/risk/var-parametric | Parametric Value-at-Risk and Conditional VaR | $0.008 |

POST /v1/risk/stress-test | Portfolio stress test across multiple scenarios | $0.008 |

POST /v1/risk/transaction-cost | Transaction cost model: commission + spread + Almgren market impact | $0.005 |

Indicators (6 endpoints)

| Endpoint | Description | Price |

|---|---|---|

POST /v1/indicators/technical | 13 technical indicators (SMA, EMA, RSI, MACD, etc.) + composite signals | $0.005 |

POST /v1/indicators/regime | Trend + volatility regime + composite risk classification | $0.005 |

POST /v1/indicators/crossover | Golden/death cross detection with signal history | $0.005 |

POST /v1/indicators/bollinger-bands | Bollinger Bands with %B, bandwidth, and squeeze detection | $0.002 |

POST /v1/indicators/fibonacci-retracement | Fibonacci retracement and extension levels | $0.002 |

POST /v1/indicators/atr | Average True Range with normalized ATR and volatility regime | $0.002 |

Statistics (12 endpoints)

| Endpoint | Description | Price |

|---|---|---|

POST /v1/stats/linear-regression | OLS linear regression with R-squared, t-stats, standard errors | $0.008 |

POST /v1/stats/polynomial-regression | Polynomial regression of degree n with goodness-of-fit metrics | $0.008 |

POST /v1/stats/cointegration | Engle-Granger cointegration test with hedge ratio and half-life | $0.008 |

POST /v1/stats/hurst-exponent | Hurst exponent via rescaled range (R/S) analysis | $0.008 |

POST /v1/stats/garch-forecast | GARCH(1,1) volatility forecast using maximum likelihood estimation | $0.015 |

POST /v1/stats/zscore | Rolling and static z-scores with extreme value detection | $0.002 |

POST /v1/stats/distribution-fit | Fit data to common distributions and rank by goodness of fit | $0.008 |

POST /v1/stats/correlation-matrix | Correlation and covariance matrices with eigenvalue decomposition | $0.015 |

POST /v1/stats/realized-volatility | Realized vol: close-to-close, Parkinson, Garman-Klass, Yang-Zhang | $0.005 |

POST /v1/stats/normal-distribution | Normal distribution: CDF, PDF, quantile, confidence intervals | $0.002 |

POST /v1/stats/sharpe-ratio | Standalone Sharpe ratio with Lo (2002) standard error and 95% CI | $0.002 |

POST /v1/stats/probabilistic-sharpe | Probabilistic Sharpe Ratio (Bailey & Lopez de Prado 2012) | $0.005 |

Portfolio (2 endpoints)

| Endpoint | Description | Price |

|---|---|---|

POST /v1/portfolio/optimize | Portfolio optimization: max Sharpe, min vol, or risk parity | $0.015 |

POST /v1/portfolio/risk-parity-weights | Equal risk contribution portfolio weights (Spinu 2013) | $0.008 |

Fixed Income (4 endpoints)

| Endpoint | Description | Price |

|---|---|---|

POST /v1/fixed-income/bond | Bond price, Macaulay/modified duration, convexity, DV01 | $0.008 |

POST /v1/fixed-income/amortization | Full amortization schedule with extra payment savings analysis | $0.005 |

POST /v1/fi/yield-curve-interpolate | Yield curve interpolation: linear, cubic spline, Nelson-Siegel | $0.015 |

POST /v1/fi/credit-spread | Credit spread and Z-spread from bond price vs risk-free curve | $0.008 |

Crypto / DeFi (7 endpoints)

| Endpoint | Description | Price |

|---|---|---|

POST /v1/crypto/impermanent-loss | Impermanent loss calculator for Uniswap v2/v3 AMM positions | $0.005 |

POST /v1/crypto/apy-apr-convert | Convert between APY and APR with configurable compounding | $0.002 |

POST /v1/crypto/liquidation-price | Liquidation price calculator for leveraged positions | $0.002 |

POST /v1/crypto/funding-rate | Funding rate analysis with annualization and regime detection | $0.005 |

POST /v1/crypto/dex-slippage | DEX slippage estimator for constant-product AMM (x*y=k) | $0.005 |

POST /v1/crypto/vesting-schedule | Token vesting schedule with cliff, linear/graded unlock, TGE | $0.005 |

POST /v1/crypto/rebalance-threshold | Portfolio rebalance analyzer: drift detection and trade sizing | $0.005 |

Live Data (2 endpoints) — paid tier, fresh market data

| Endpoint | Description | Price |

|---|---|---|

POST /v1/live/volatility | Live realized volatility (7d/30d/90d) + regime for a crypto asset | $0.01 |

POST /v1/live/funding-rates | Live perpetual funding rate + annualized carry for a crypto asset | $0.005 |

Paid from the first call (not part of the free tier); 20 free calls/IP/day. See QuantOracle Live.

Watch — position monitoring (6 endpoints)

| Endpoint | Description | Price |

|---|---|---|

POST /v1/watch/trial | Free 48-hour trial monitor (one per IP per 30 days) | Free |

POST /v1/watch/position | 24/7 monitoring of a perp position for 30 days | $5.00 |

POST /v1/watch/extend | Extend or upgrade a monitor by 30 days | $5.00 |

PATCH /v1/watch/{id} | Update position params (direction/entry/size/collateral/mmr/webhook/thresholds) | Free |

GET /v1/watch/{id} | Live status + alert history (token auth) | Free |

DELETE /v1/watch/{id} | Cancel a monitor | Free |

Priced per monitor, not per call. See QuantOracle Watch.

FX / Macro (7 endpoints)

| Endpoint | Description | Price |

|---|---|---|

POST /v1/fx/interest-rate-parity | Interest rate parity calculator with arbitrage detection | $0.005 |

POST /v1/fx/purchasing-power-parity | Purchasing power parity fair value estimation | $0.005 |

POST /v1/fx/forward-rate | Bootstrap forward rates from a spot yield curve | $0.005 |

POST /v1/fx/carry-trade | Currency carry trade P&L decomposition | $0.005 |

POST /v1/macro/inflation-adjusted | Nominal to real returns using Fisher equation | $0.002 |

POST /v1/macro/taylor-rule | Taylor Rule interest rate prescription | $0.002 |

POST /v1/macro/real-yield | Real yield and breakeven inflation from nominal yields | $0.002 |

Time Value of Money (5 endpoints)

| Endpoint | Description | Price |

|---|---|---|

POST /v1/tvm/present-value | Present value of a future lump sum and/or annuity stream | $0.002 |

POST /v1/tvm/future-value | Future value of a present lump sum and/or annuity stream | $0.002 |

POST /v1/tvm/irr | Internal rate of return via Newton-Raphson | $0.005 |

POST /v1/tvm/npv | Net present value with profitability index and payback period | $0.002 |

POST /v1/tvm/cagr | Compound annual growth rate with forward projections | $0.002 |

Simulation (1 endpoint)

| Endpoint | Description | Price |

|---|---|---|

POST /v1/simulate/montecarlo | GBM Monte Carlo with contributions/withdrawals, up to 5000 paths | $0.015 |

Composite Endpoints (paid-only)

Higher-level endpoints that combine multiple calculations into a single call. Same math as the individual endpoints -- just packaged for common agent workflows. No free tier.

| Endpoint | Description | Replaces | Price |

|---|---|---|---|

POST /v1/backtest/strategy | Run SMA crossover, RSI mean reversion, momentum, or Bollinger breakout backtest | 10+ indicator + risk calls | $0.10 |

POST /v1/options/spread-scan | Scan and rank vertical spreads by risk/reward | 8-16 options/price calls | $0.05 |

POST /v1/portfolio/rebalance-plan | Generate trade list to hit target weights with cost estimate | portfolio/optimize + transaction-cost | $0.05 |

POST /v1/options/strategy-optimizer | Rank top options strategies given outlook + volatility view | options/strategy + payoff-diagram | $0.08 |

POST /v1/hedging/recommend | Rank cheapest effective hedges (protective put, collar, futures, partial) | options/price + Greeks | $0.04 |

POST /v1/risk/full-analysis | Complete risk tearsheet: Sharpe, Sortino, VaR, Kelly, drawdown, Hurst, CAGR | 7 individual calls | $0.04 |

POST /v1/portfolio/health | Portfolio health check: risk, correlation, rebalance, stress test | 6 individual calls | $0.04 |

POST /v1/trade/evaluate | Trade evaluation: sizing, risk/reward, Kelly, costs, regime, signals, verdict | 5 individual calls | $0.025 |

POST /v1/pairs/signal | Pairs trading signal: cointegration, Hurst, z-score, half-life, hedge ratio | 4 individual calls | $0.025 |

POST /v1/indicators/regime-classify | Trend, vol regime, RSI, direction, strategy suggestion | technical + regime + realized-vol | $0.015 |

Example: Agent Backtest Workflow

A typical agent backtest chains multiple QuantOracle calls per iteration:

1. /v1/indicators/technical -- generate signals (SMA, RSI, MACD)

2. /v1/risk/position-size -- size the trade (fixed fractional)

3. /v1/risk/transaction-cost -- estimate execution costs

4. /v1/options/price -- price the hedge (Black-Scholes)

5. /v1/risk/portfolio -- compute running Sharpe, drawdown, VaR

6. /v1/stats/probabilistic-sharpe -- is the Sharpe statistically significant?

7. /v1/tvm/cagr -- compute CAGR of the equity curve

Each call is a pure calculator -- no state, no side effects, no API keys.

Strategy Optimizer (1,200+ calls)

examples/strategy_optimizer.py is a full walk-forward parameter optimizer that demonstrates heavy API usage:

| Phase | What it does | API calls |

|---|---|---|

| Parameter Sweep | Test 180 lookback/rebalance/RSI combinations across 8 assets | ~1,080 |

| Deep Analysis | 22 risk metrics + VaR + Kelly + Monte Carlo on top 3 configs | ~60-80 |

| Options Overlay | Price covered calls across 6 assets x 4 expiries x 5 strikes | ~100-150 |

| Pairs Analysis | Cointegration scan + Hurst exponent on 45 asset pairs | ~50-70 |

pip install requests

python examples/strategy_optimizer.py

A single run makes ~1,200-1,500 API calls. At paid rates that's ~$6-8 USDC. The same calculations done by an LLM in-context would cost $12-60 in tokens (Sonnet to Opus), take 4x longer, and get 15-30% of the complex math wrong.

Self-Hosting

# Clone and run locally

git clone https://github.com/QuantOracledev/quantoracle.git

cd quantoracle

pip install fastapi uvicorn

uvicorn api.quantoracle:app --host 0.0.0.0 --port 8000

# Docker

docker compose up -d

# Docs at http://localhost:8000/docs

Accuracy

Every endpoint is tested against published analytical solutions:

- 120 citation-backed benchmarks (Hull, Wilmott, Bailey & Lopez de Prado, Goldman-Sosin-Gatto, Taylor, Fisher, Markowitz)

- 65+ integration tests covering all 63 calculators

- Pure Python math -- no numpy/scipy, zero native dependencies

- Deterministic: same inputs always produce the same outputs

Run the verification suite yourself:

python tests/accuracy_benchmarks.py https://api.quantoracle.dev

Architecture

quantoracle/

api/quantoracle.py -- FastAPI app, 63 calculators + 11 composites, pure Python math

worker/src/index.ts -- Cloudflare Worker: rate limiting + x402 payments (Base + Solana)

mcp-server/src/index.ts -- MCP server: 80 tools (incl. live data + Watch) over Streamable HTTP

cli/ -- quantoracle-cli: all endpoints in the terminal (npm)

tests/

test_integration.py -- 65 integration tests (all endpoints, live API)

accuracy_benchmarks.py -- 120 citation-backed accuracy tests

Stack: FastAPI + Pydantic | Cloudflare Workers + KV | MCP (Streamable HTTP) | x402 + CDP Facilitator | USDC on Base and Solana

License

MIT -- use QuantOracle however you want.